Your investment questions answered

Although we know many of you are experienced and pension-savvy, it’s not everyone’s cup of tea. So we thought we’d collate the things we get asked the most here.

What is meant by investments in the Fund?

Investments are the funds where your pension contributions are placed (invested) to help grow your Individual Account over time.

The size of your Individual Account will depend on the level of contributions paid and how your investments perform.

What investment options do I have?

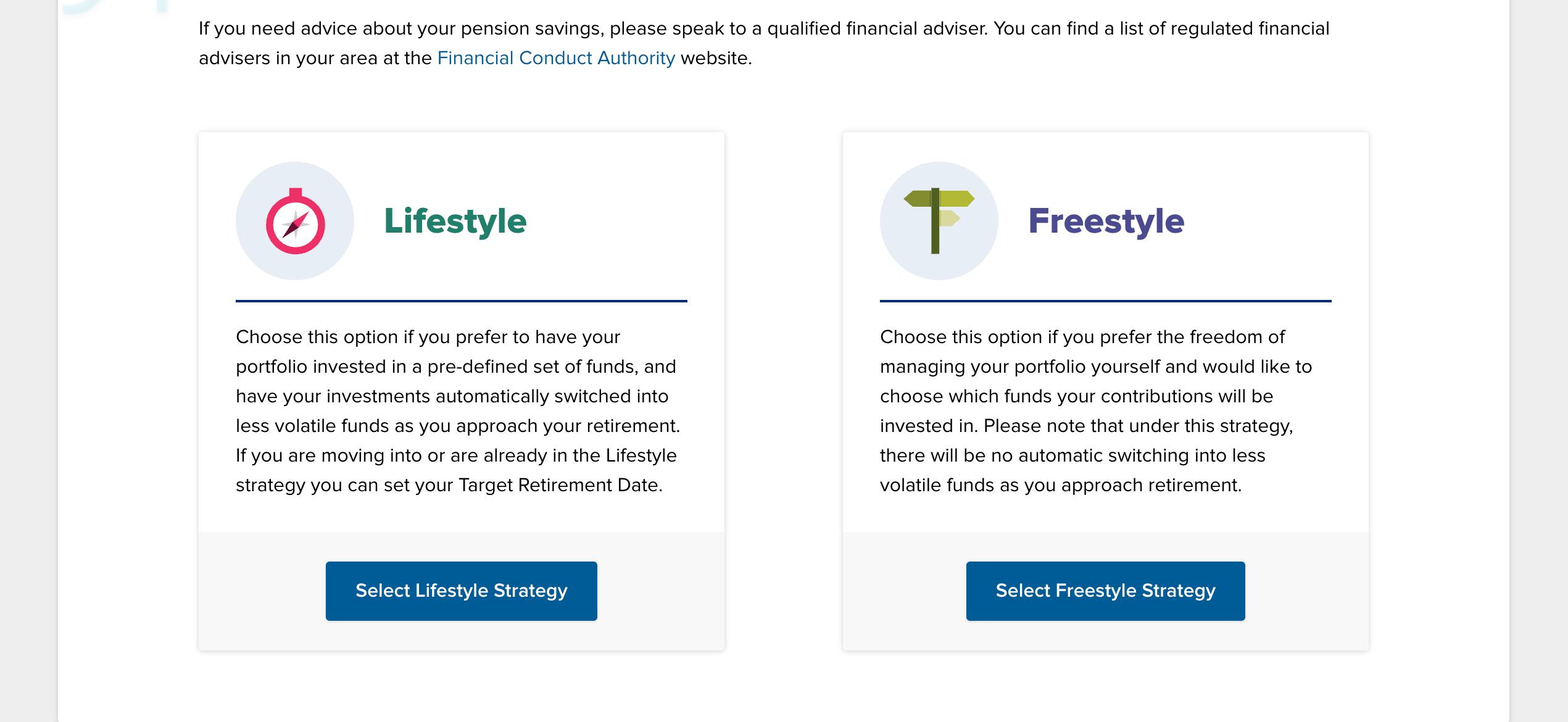

You have two main approaches for investing your Individual Account:

Mercer SmartPath (also called “Lifestyle” on OneView): an investment strategy that automatically adjusts your investments based on your target retirement date and how you plan to take your retirement benefits. There are three SmartPath strategies –drawdown, annuity, or cash – and each one is aligned with a different way of taking your pension savings.

Self Select (also called “Freestyle” on OneView): you can choose your own investment funds from the range of options on offer.

What are the Mercer SmartPath strategies?

There are three Mercer SmartPath strategies, which will initially invest in higher risk, higher potential growth investments until you are around eight years from retirement (more information is available in the Investment Guide). The Mercer SmartPath strategies will then gradually switch your investments into funds designed to be suitable for the way you are planning to take your pension savings.

The three Mercer SmartPath strategies are:

Target Drawdown: Suitable if you plan to draw an income flexibly in retirement.

Target Annuity: Suitable if you plan to buy a guaranteed income for life (annuity).

Target Cash: Suitable if you plan to take your pension savings as a single cash lump sum.

More information on the Mercer SmartPath strategies is available in the Investment Guide and in the Mercer SmartPath video.

Can I choose a mix of Mercer SmartPath and Self Select funds?

No, Mercer SmartPath and Self Select investments can’t be mixed for the same Individual Account. You must invest 100% of your Individual Account in the Mercer SmartPath strategies, or 100% in Self Select funds.

If you choose Mercer SmartPath, you may split your Individual Account across the three different Mercer SmartPath strategies, provided the splits add up to 100%.

Can I change my investment choices?

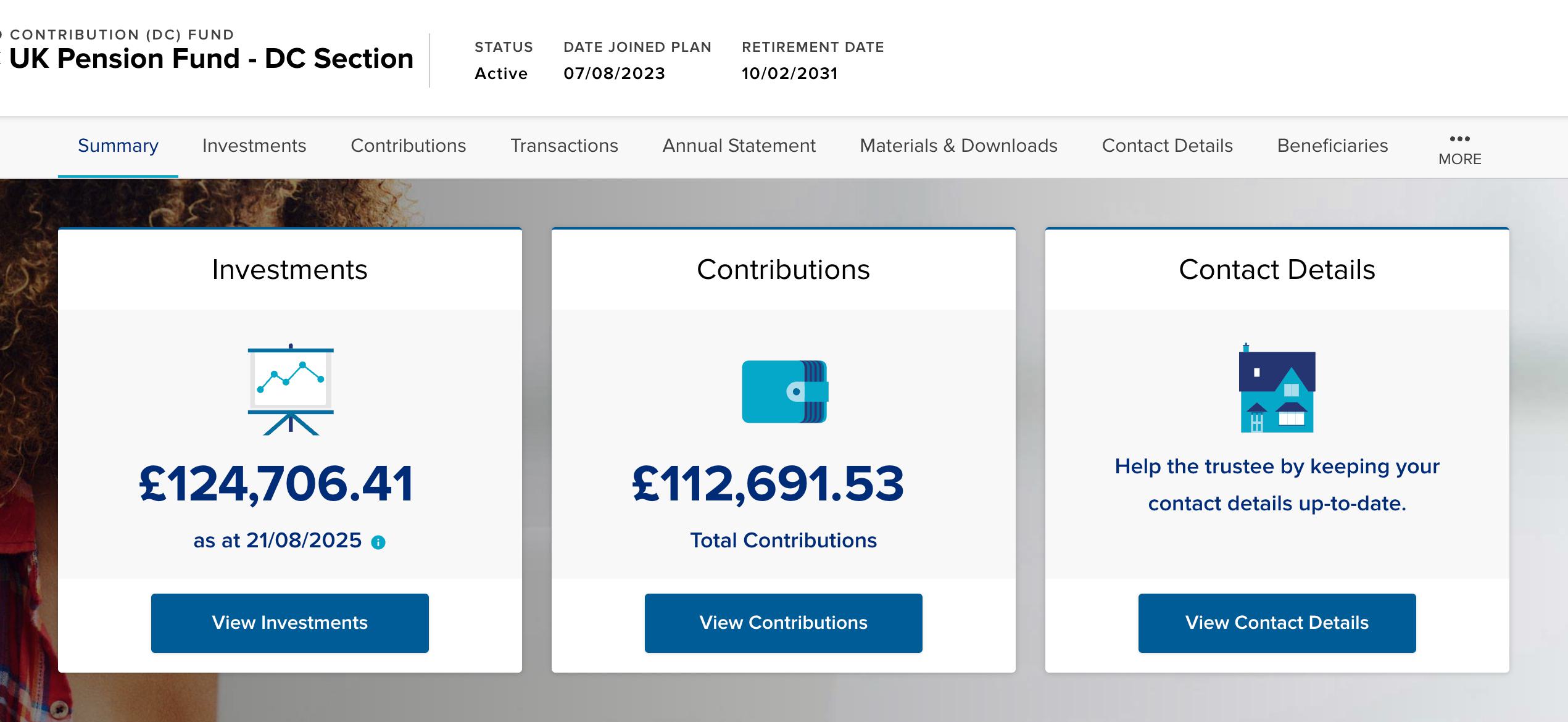

Yes, you can change how your Individual Account is invested at any time via OneView.

How do I log into OneView?

The easiest way is to click here and follow the onscreen instructions. Alternatively:

If you're currently employed by Marsh, log in via ‘My Quick Links’ on Colleague Connect.

If you're a former employee, you can access OneView directly with your login details. If you’ve forgotten your credentials or need help logging in, simply follow the onscreen instructions.

It’s always good to bookmark our Fund website pensions.uk.mmc.com – from here you can click the ‘Log into OneView’ button at the top of the page.

How do I review and make changes to my investment options?

It’s simple to do – once you’ve logged into OneView, click on ‘View details’, then:

1. Click on ‘View investments’.

2. Scroll down the page and click on ‘Investment choices’.

3. Click ‘Select Lifestyle Strategy’ to check and change your investments in this strategy, which is set as the default.

4. Alternatively, click ‘Select Freestyle Strategy’ if you manage your investments yourself. We strongly recommend you speak to an FCA-regulated financial adviser before making any major changes to your investments.

Please note that on OneView, the Mercer SmartPath strategies are called “Lifestyle” and the Self Select funds are called “Freestyle”.

What if I don’t make an investment decision?

If you don’t make an active decision, your Individual Account will be invested in the Fund’s default investment option – Mercer SmartPath Target Drawdown, with a default target retirement date of your 65th birthday.

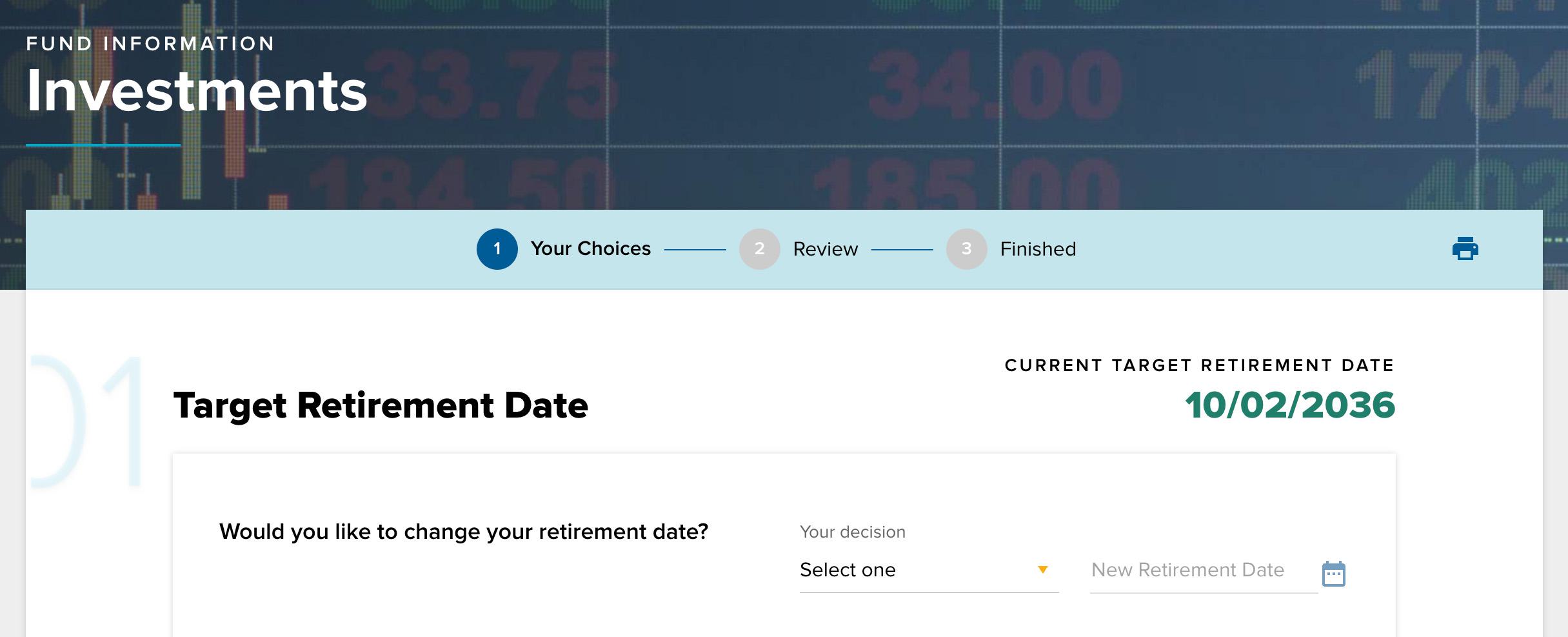

What is my target retirement date?

This only applies if you’re invested in Mercer SmartPath and is the date you expect or plan to start taking your pension savings. Your default target retirement date in the Fund is your 65th birthday, unless you’ve selected a different date on OneView.

If you choose Self Select, you don’t need to set a target retirement date. Whilst the Fund’s default retirement age is 65, you can still take your retirement benefits earlier or later, in line with pension rules, to suit your own circumstances.

Why do I need to set a target retirement date?

This date is important because it determines how your pension savings are invested if you’re invested in one of the Mercer SmartPath strategies, as they automatically adjust your investments based on how many years you have left until your target retirement date.

Your target retirement date tells us when to start this adjustment to your investments. If it’s wrong, your money could be moved too early or too late, which might affect how much money you have when you come to retire.

Don’t forget, if you choose Self Select you don’t need to set a target retirement date – the Fund’s default retirement age is 65, but you can still take your pension savings earlier or later than this to suit your circumstances (in line with pension rules).

You can change your target retirement date at any time via OneView.

How can I change my target retirement date?

You should check and update this if needed to ensure your investments match your retirement plans. Once you’ve logged into OneView, click on ‘View details’, then: Click on ‘View investments’.

Scroll down the page and click on ‘Investment choices’.

Click ‘Select Lifestyle Strategy’ and under ‘Target Retirement Date’ you can add a ‘New Retirement Date’.

Is there a fee to change my investment options?

No, there is no administration fee for changing your investment options. However, when you switch between investment funds, there may be small buying and selling costs involved which are reflected in the investment fund unit price. As a result, the price of the investment fund units* may go up or down each day to cover these buying and selling costs. These costs aretypically small and exist to protect the value of existing investors’ pension savings when these changes happen.

* Investment fund units are essentially a small share or part of an investment fund that you own – when you invest in a fund, you are buying these parts, or “units”, which represent a proportional share of the investment fund’s total assets.

What are the charges for investing my Individual Account?

An annual management charge is automatically deducted from the value of your Individual Account by the investment manager. Indicative information on the charges (known as Total Expense Ratio) is set out in the Investment Guide and specific information on the annual charges for each fund is available in the fund factsheets.

What types of investment funds are available as Self Select options?

There’s a wide range of investment funds available, including cash, bond, equity, and specialist funds. Each fund has a specific investment objective and performance target, and different risk and return profiles. A list of the funds available, with a description of the fund’s aim, can be found in the Investment Guide.

Where can I find information on all the Fund’s investment options?

You can find details of all the investment options available to you in the Investment Guide.

What risks should I be aware of when investing?

All investments carry risk, but there are different types of risk – you need to decide how much of each type of risk you’re prepared to take. Here are some types of risk to consider when choosing your investments:

Capital risk: investments may fall in value and not recover. This could happen with equities, bonds, alternative assets and even cash funds.

Inflation risk: investments may keep up with the cost of living.

Pension conversion risk: the cost of buying an annuity can vary and moves broadly in line with bonds and gilts (government bonds).

Default risk: the risk that bond issuers fail to repay capital when due.

Interest rate risk: The risk of potential investment losses due to fluctuations in interest rates, particularly affects bonds and gilts. When interest rates rise, the value of existing bonds typically falls because new bonds are issued at higher rates, making older bonds less attractive (and vice versa).

How can I keep track of my investments?

You can use OneView to check your investment choices, review your contributions and transaction history, and change your investment strategy (where appropriate).

Once you’ve logged into OneView, click on ‘View details’, then you can:

1.Click on ‘View investments’ to check how you’re invested.

2. View ‘Personalised Account Growth’ to see how your Individual Account has changed over time.

3. Go to ‘Investment Choices’ to make changes to your investment strategy.

4. Take a look at ‘Contributions’ to review the contributions made to your Individual Account.

5. Find details under ‘Transactions’ of the transactions that have happened on your Individual Account.

Can I invest my future contributions differently to my current investments?

Yes, if you’re an active member of the Fund, you can choose to invest your future contributions in a different way to your existing investments.

You can do this on OneView:

Go to ‘Investments’, then to ‘Resources’ and click on ‘Investment Choices’.

From here you can select a strategy – ‘Lifestyle’ (SmartPath) or ‘Freestyle’ (Self Select) – and for the investment options given for your chosen strategy, you can choose the percentage(s) for ‘Current Investments’ and ‘Future Investments’, as required.

What should I do if I’m unsure about my investment choices?

You should regularly review your investment choices to ensure they match your retirement plans.

For help:

You can find out more about your retirement options and the support available to you on our retirement page. If you’re age 40 or over, you have access to Destination Retirement, a free online retirement planning and advice service.

If you’re over age 50, you can get free, impartial guidance from the Government’s Pension Wise service: https://www.moneyhelper.org.uk/en/pensions-and-retirement/pension-wise.

For personalised advice, consult an FCA-regulated financial adviser. Find more information at: https://www.moneyhelper.org.uk/en/getting-help-and-advice/financial-advisers/choosing-a-financial-adviser.

What role does the Trustee play in managing the Fund’s investments?

The Trustee operates a robust governance framework and selects the investment options offered after taking professional advice from their Investment Adviser. The Trustee keeps these options under regular review and the Fund’s Investment Committee meets quarterly to monitor investment performance and risks, reporting findings to the Trustee for ongoing oversight and decision-making.

As you’re in a Defined Contribution pension arrangement, the value of your Individual Account depends on contributions paid in and the performance of your chosen investments, with members bearing all investment risk (and all investments come with risk). The Trustee doesn’t guarantee investment returns and isn’t liable for any investment losses. You have the option to change your investment choices or transfer to another pension arrangement at any time if you’re dissatisfied with investment performance.

Where can I find more detailed information?

The Fund website has lots of resources, including the Investment Guide, and contains regular updates.

Contact the Fund Administrator at pensionuk.aptia-group.com for any other questions.